Europe Pet Food Ingredient Market Size

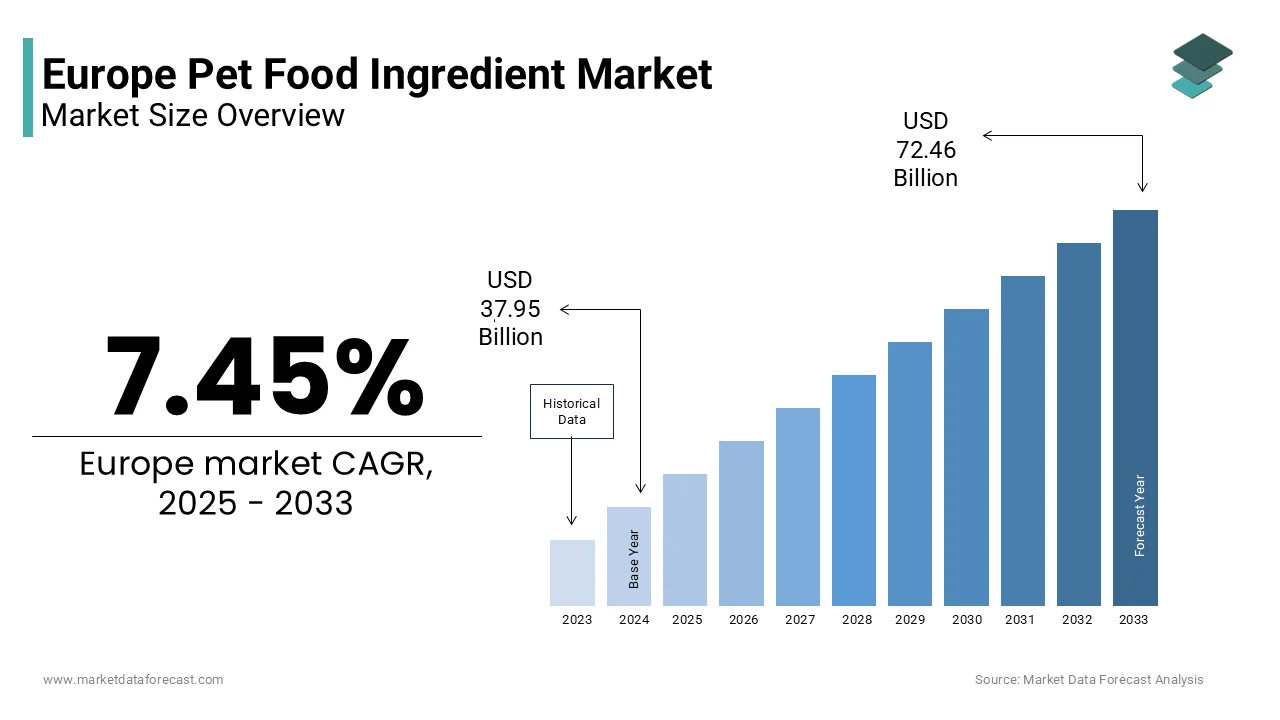

The Europe pet food ingredient market size was valued at USD 37.95 billion in 2024 and is projected to reach USD 72.46 billion by 2033, growing at a CAGR of 7.45% from USD 40.78 billion in 2025.

Pet food ingredient refers to the raw materials and functional additives used in the formulation of nutritionally balanced diets for companion animals, primarily dogs and cats. These ingredients range from animal proteins and plant-based carbohydrates to vitamins, minerals, probiotics, and novel functional components such as insect proteins and algae-based omega fatty acids. In Europe, pet food formulation is governed by stringent safety, traceability, and labelling regulations under the European Pet Food Industry Federation and EU Feed Hygiene Regulation, which mandate full ingredient disclosure and prohibit the use of certain by-products and artificial additives. According to sources, a substantial portion of households in the European Union own at least one pet, with cats and dogs remaining the most common companion animals. This figure has remained consistently high in recent years. As per the European Commission’s Farm to Fork Strategy, sustainability and circularity now extend to pet nutrition, driving demand for ethically sourced, low-impact ingredients. Furthermore, Pet owners increasingly focus on the ingredients in pet food, showing a strong preference for natural composition and transparency when making purchasing decisions. In this context, pet food ingredients are no longer mere nutritional fillers but strategic elements reflecting evolving consumer values around health, ethics, and environmental stewardship.

MARKET DRIVERS

Rising Humanisation of Pets and Demand for Premium, Human-Grade Ingredients

The deepening emotional bond between Europeans and their companion animals has caused a shift toward human-grade and clean-label pet food formulations, which fuels the growth of the European pet food ingredients market. This directly increases demand for high-quality and traceable ingredients. According to research, the European pet food market reflects a pervasive trend where pet owners increasingly view their companion animals as integral family members, driving demand for high-quality food options. This trend is particularly strong in Western and Northern Europe. Pet owners in Europe and globally show a strong and growing preference for pet foods with natural ingredients, actively seeking to avoid artificial preservatives, colours, and certain by-products. Consequently, pet food manufacturers are reformulating products with identifiable proteins like chicken, duck or salmon and functional botanicals such as turmeric and blueberries. European Union feed legislation, aligned with circular economy goals, increasingly permits the responsible and safe incorporation of approved human food surplus streams as sustainable ingredients in pet food production. This regulatory flexibility enables brands to appeal to both health-conscious and eco-aware consumers, transforming ingredient sourcing into a core differentiator in Europe’s premium pet care landscape.

Stringent EU Regulations on Feed Safety and Ingredient Transparency

The region’s rigorous regulatory framework for animal feed significantly shapes ingredient selectionprioritisingng safety, traceability, and ethical sourcing to ultimately boost the expansion of the European pet food ingredients market. The EU Feed Hygiene Regulation (EC No 183/2005) mandates full traceability from raw material origin to finished product, requiring suppliers to document sourcing, processing, and contamination controls. EU feed safety monitoring in 2023 consistently showed high compliance rates for residues of veterinary medicines and pesticides in animal products and feed materials across member states and imported goods, building consumer confidence in the regulatory framework. The European Commission also enforces a positive list of authorised feed materials, excluding many cost-effective but controversial ingredients such as certain rendered meats and synthetic antioxidants. Regulatory trends in the European Union indicate a strong push for greater alignment of animal health and welfare standards for imported animal products with domestic EU production standards, a policy often discussed in the context of trade agreements. Additionally, European Union legislation, specifically Regulation (EC) No 767/2009, requires a comprehensive and transparent approach to pet food labelling, ensuring all ingredients are declared clearly to avoid misleading consumers and enable informed choices. These rules elevate compliance costs but also build market trust, making regulatory adherence a non-negotiable entry point for ingredient suppliers in Europe.

MARKET RESTRAINTS

Restrictive Legislation on Novel and Insect-Based Protein Sources

Novel protein sources, particularly insect meal, are hampered by slow regulatory approval and restrictive labelling requirements in the European Union, despite their sustainability potential, which in turn restricts the growth of the European pet food ingredients market. Diverse insect species and processed insect ingredients are increasingly permissible for use in EU pet food, adhering to general feed safety and hygiene standards, with no specific limitations on the number of species or overall protein content. The approval process under Regulation (EU) 2019/1009 requires extensive safety dossiers and environmental impact assessments, delaying commercialisation. The European Food Safety Authority (EFSA) is actively conducting safety assessments on a number of pending applications for various insect-derived ingredients intended for human consumption, reflecting ongoing regulatory scrutiny and interest in expanding the range of approved novel foods. Furthermore, labelling rules compel manufacturers to list insect ingredients as processed animal protein, a term historically associated with bovine spongiform encephalopathy, triggering consumescepticismsm. The widespread adoption of these promising sustainable proteins will be limited until regulatory processes are simplified and consumers are better informed.

High Volatility in Raw Material Prices and Supply Chain Disruptions

Persistent cost instability due to global fluctuations in agricultural commodities and geopolitical supply chain risks inhibits the expansion of the European pet food ingredient market. The price of key inputs such as poultry meal, fishmeal, and pea protein has risen. The war in Ukraine disrupted sunflower meal and wheat supplies, critical carbohydrate sources, forcing European formulators to seek costly alternatives. Many pet food producers have experienced ingredient shortages. Additionally, new regulations are coming into effect that impose due diligence requirements on certain soy and palm oil derivatives. These pressures disproportionately affect small and medium pet food brands with limited purchasing power, stifling innovation and limiting access to premium ingredients. Price volatility will persist, challenging market stability and product consistency, unless strategic stockpiling or vertical integration strategies are implemented.

MARKET OPPORTUNITIES

Expansion of Functional and Therapeutic Ingredients for Pet Health Management

The growing focus on preventive pet healthcare is driving demand for functional ingredients that support digestion, immunity, joint health, and cognitive function, and thereby provides new opportunities for the growth of the European pet food ingredients market. According to research, a notable share of dogs and cats in the EU suffer from age-related or chronic conditions such as arthritis, obesity or renal insufficiency, creating a market for clinically supported nutraceuticals. Ingredients like glucosamine,, neochondroitin,itin, omega-3 fatty acids from algae and probiotics such as Enterococcus faecium are increasingly incorporated into therapeutic diets. Regulatory developments further enable this trend. Companies like Royal Canin and Hill’s leverage veterinary partnerships to co-develop condition-specific formulas, embedding ingredients like green-lipped mussel extract or prebiotic fibres. European pet owners are increasingly valuing long-term health and well-being over simple dietary needs, making functional ingredients key drivers for product differentiation and premium pricing within the pet care industry.

Adoption of Circular Economy Principles in Ingredient Sourcing

Pet food manufacturers in the region are increasingly leveraging food industry co-products and upcycled streams as sustainable and cost-effective ingredients in alignment with the EU Circular Economy Action Plan, which provides fresh prospects for the European pet food ingredients market. A notable amount of food surplus originally meant for human consumption, including materials like spent grains, fruit pulp from juice production, and bakery waste, is being repurposed into pet food. Many companies in the pet food industry are incorporating upcycled ingredients into their product lines as a standard practice. Specific types of former foodstuffs, such as unsold dry pasta or breakfast cereals that do not contain meat or fish components, have been approved for safe use as components in pet food. This regulatory shift supports brands that market “rescued ingredient” kibbles with notable carbon footprint reductions compared to conventional formulas. “Sustainable pet nutrition in Europe is pivoting to circular sourcing, fueled by green consumerism and policies that promote waste valorisation.

MARKET CHALLENGES

Shortage of Skilled Formulators and Regulatory Experts in Pet Nutrition

There is a critical gap in specialised professionals who can navigate complex nutritional science, regulatory compliance, and consumer trends simultaneously, which ultimately constrains the growth of the European pet food ingredients market. According to sources, the pet food industry in the EU experiences a relatively limited number of highly specialised professionals in pet food formulation. Small and emerging brands often lack in-house expertise to interpret evolving feed legislation or design balanced diets with novel ingredients like algae or insect protein. There is a general trend within the pet food sector for small and medium-sized enterprises (SMEs) to rely on external consultants for specialised formulation needs, which can impact product development timelines and expenditures. Furthermore, the European Food Safety Authority requires detailed nutritional adequacy dossiers for new complete feeds, a process demanding deep knowledge of species-specific requirements and analytical validation. Innovation in sustainable and functional pet food development, which demands significant technical precision, will remain stifled due to a skills gap, absent effective coordinated academic programs and industry collaboration.

Consumer Mistrust Due to Inconsistent Labelling and Greenwashing Claims

Inconsistent iingredient labellingand unsubstantiated sustainability claims continue to erode consumer trust, despite regulatory efforts, which challenges the expansion of the European pet food market. The European Consumer Organisation points out that a considerable number of pet owners struggle with understanding terms like “natural,” “holistic,” and “premium” on pet food packaging, as these terms currently do not have a standard legal definition under EU law. Brands often highlight single attributes, such as grain-free or plant-based, while omitting critical nutritional trade-offs, leading to diet imbalances. European Union market monitoring activities and related reports indicate a significant trend of products across e-commerce platforms, including those in the pet food sector, making unsubstantiated or potentially misleading environmental claims. Besides, the mandatory ingredient list, while transparent, is often overshadowed by prominent front-of-pack marketing that emphasises emotional appeal over factual composition. This information asymmetry fuels scepticism, particularly among educated urban pet owners who demand scientific backing for health and sustainability assertions. Market growth will remain modest until consistent, enforced standards for nutritional and environmental claims, like those for human food, are implemented to build consumer trust and brand credibility.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

7.45% |

|

Segments Covered |

By Ingredient Type, Form, Product Type, Animal, Source, Nature, and Region |

|

Various Analyses Covered |

Global, Regional, & Country Level Analysis; Segment-Level Analysis; DROC, PESTLE Analysis; Porter’s Five Forces Analysis; Competitive Landscape; Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, and the Czech Republic |

|

Market Leaders Profiled |

Nestle Purina PetCare (US), Mars Petcare (US), Hill’s Pet Nutrition (US), Diamond Pet Foods (US), Blue Buffalo (US), Spectrum Brands (US), WellPet (US), Merrick Pet Care (US), Royal Canin (FR) |

SEGMENTAL ANALYSIS

By Ingredient Type Insights

The meat and meat products segment held the largest share of 52.6% of the European pet food ingredient market in 2024. The leading position of the meat and meat products segment is attributed to the biological requirement of dogs and cats for high-quality animal protein as obligate or facultative carnivores, reinforced by strong consumer preference for meat-centric formulations. Dogs and cats require essential amino acids such as taurine, arginine,ne and methionine that are most bioavailable in animal-derived proteins. Pet foods often feature meat or meat meal as a primary ingredient to meet nutritional guidelines. Regulatory standards specify minimum protein levels for dog and cat food, with animal sources favoured for digestibility and amino acid profile. Studies indicate that pet foods with poultry or fish as the main ingredient may have higher protein digestibility than plant-based options. Furthermore, most pet owners view “real meat” as an important consideration when choosing pet food. This scientific and consumer alignment ensures meat remains the foundational ingredient across premium and mainstream pet food categories throughout Europe. European pet owners increasingly reject generic “meat meal” inin favourf transparently sosourcedddentifiable proteins like chicken,, uck, lamb or salmon. According to sources, a share of surveyed pet owners stated they avoid products with unspecified animal byproducts. This demand has pushed manufacturers to reformulate with human-grade or free-range meats. The European Commission’s updated feed lalabellingules now require specific identification of protein sources such as “dehydrated turkey protein” instead of vague terms, enhancing consumer trust. Brands highlight traceable meat from EU farms on packaging supported by blockchain verification. Furthermore, the Farm to Fork Strategy incentivises the use of surplus human food-grade meat streams, reducing waste while meeting premium expectations. As ethical sourcing and ingredient clarity become non-negotiable, meat and meat products sustain their leadership through both nutritional necessity and market differentiation.

The additives segment is on the rise and is expected to be the fastest-growing segment in the market by witnessing a CAGR of 8.4% from 2025 to 2033. The rapid expansion of the additives segment is propelled by the rising demand for functional and therapeutic pet nutrition, and regulatory endorsement of novel and precision nutrition additives. European pet owners are increasingly seeking foods that support specific health outcomes such as joint mobility, digestive health,, and cognitive function , driving demand for scientifically backed additives. According to research, a notable share of dogs and cats in the EU suffer from chronic conditions that benefit from targeted nutrition. Ingredients like glucosamine, chondroitin, probiotics, ega-3 fatty acids and antioxidants are now standard in premium and veterinary diets. The European Commission permits health claims for certain feed additives under Regulation EC No 1831/2003 if supported by dossiers demonstrating efficacy. Companies leverage clinical trials to validate additive performance, creating trust and justifying premium pricing. This shift from basic nutrition to proactive health management is transforming additives from minor components into key value drivers. The European Food Safety Authority has streamlined evaluation pathways for innovative additives that address emerging pet health needs. The European Commission subsequently authorised these for use in pet food under strict purity and dosage criteria. This regulatory openness enables brands to differentiate with science-led formulations. Moreover, the EU’s antimicrobial resistance action plan encourages probiotic use as an alternative to growth promoters, further boosting adoption. The increasing life spans and owners’ demand for longevity are driving accelerated growth for functional additives across Europe, positioning them at the intersection of science and sustainability.

By Animal Insights

The dog segment led the European food ingredient market and captured a share of 48.6% in 2024. The prominence of the dog segment is because of the high number of dog-owning households and their larger average food consumption per animal. Large and giant breeds, which are popular in countries like Germany and the UK, can consume notable grams dai,, requiring substantial protein and energy-dense formulations. Furthermore, dogs are more likely to receive multiple food formats,including kibble wet food, treats and supplements, treating diversified ingredient usage. As per research, most dog owners purchase at least two product types regularly. This volume effect,, combined with broad demographic appeal, ensures dogs remain the largest driver of ingredient procurement across Europe’s pet food manufacturing landscape. Dogs exhibit exceptional physiological diversity with h several recognised breeds ranging from Chihuahuas to Great Danes, each with distinct metabolic and nutritional requirements. Puppies, senior dogs and working breeds also demand tailored formulations. Puppy foods require higher calcium and DHA , while senior formulas emphasise joint support and reduced phosphorus. Besides, active and sporting dogs prevalent in Nordic countries consume high-protein, high-fat diets with added carnitine and taurine. This complexity drives demand for a wider array of functional ingredients, fats and micronutrients compared to other companion animals, ls solidifying dogs as the most ingredient-intensive segment in the European market.

The cat segment is expected to exhibit a noteworthy CAGR of 7.9% from 2025 to 2033, owing to rising urban cat ownership and premiumization of feline nutrition, and increased focus on preventive health and urinary wellness.

Cats are increasingly favoured in urban European households due to their space efficiency and independent nature. Cat ownership is increasing in major cities. The rate of new cat owners is higher in high-density, apartment-based living environments. Also, the growth in the number of urban pet cats is currently faster than the growth in the number of urban pet dogs. Constraints related to apartment living are a significant factor in pet choice. Urban cat owners also spend more per pet. According to studies, cat food expenditure per household rose, driven by premium wet food and functional kibble purchases. Cats are obligate carnivores requiring taurine and arachidonic acid, and preformed vitamin A, all of which must come from animal sources, pushing demand for high-quality meat and fish ingredients. Brands highlight single-source proteins and grain-free recipes catering to this discerning demographic. As urbanisation continues and disposable incomes rise, elite nutrition is becoming a h-marginin growth engine across Western and Southern Europe. Cats are prone to urinary tract issues, dental disease, and obesity, making preventive nutrition a priority for owners and veterinarians. The incidence of chronic kidney disease generally increases as cats age, making it a common health concern in senior feline populations. Feline lower urinary tract disorders are prevalent, and affected cats often experience recurring episodes of clinical signs regardless of the specific cause. This has driven demand for therapeutic ingredients like cranberry extract, DL methionin,e nd controlled magnesium levels in mainstream foods. Furthermore, probiotics for gut health and omega-3 for skin conditions are increasingly standard. Companies invest in feline-specific research. This science-led approach c,, combined with rising veterinary engagement ensures sustained innovation and ingredient diversification in the cat segment.

By Source Insights

In 2024, the animal-based segment held the leading share of 61.7% of the European pet food ingredient market. The dominance of the animal-based segment is driven by the carnivorous physiology of primary companion animals and strong consumer preference for meat-centric diets. Cats are obligate carnivores requiring preformed taurine, vitamin A and arachidonic acid w,, which are naturally abundant only in animal tissues. Dogs, while omnivorous t,, thrive on high-quality animal protein for optimal muscle maintenance and immune function. The European pet food industry, represented by organisations like the European Pet Food Industry Federation, formulates most complete cat and dog foods with a high proportion of protein derived from animal sources to meet species-appropriate nutritional needs. European regulations require specific levels of essential nutrients like taurine in all complete cat foods to prevent serious health issues, with appropriate supplementation from various sources, including both animal hydrolysates and synthetic forms. Consumer perception in the pet food market strongly links the presence of “real meat” with high quality and pet health, a trend that significantly influences product development and demand. This nutritional and perceptual alignment ensures animal-based ingredients remain dominant despite sustainability pressures. A significant shift has occurred in Europe: while animal ingredients still lead the market, both consumers and regulatory bodies are now strongly opposed to unspecified rendered meals and low-grade by-products. The EU Feed Hygiene Regulation requires full traceability and prohibits Category 1 and 2 animal by-products in pet food. As a result, manufacturers source high-quality fresh or dehydrated meats from EU-approved slaughterhouses. Brands respond by using named proteins like salmon hydrolysate or chicken liver, supported by QR code traceability. This quality upgrade trend has increased the average cost but also the value perception of animal-based ingredients, making them central to premiumization strategies across Europe.

The plant derivatives segment is predicted to witness the highest CAGR of 9.1% from 2025 to 2033 due to the demand for sustainable and hypoallergenic alternative protein sources, and innovation in functional botanicals and prebiotic fibres. European pet owners are increasingly seeking plant-based ingredients to reduce environmental impact and address pet food allergies. In addition, brands are incorporating pea, ahickpea protein as partial meat substitutes. Companies offer certified vegan pet foods using balanced amino acid profiles from legumes and algae. The European Commission’s Circular Economy Action Plan supports the use of upcycled fruit pomace and spent grains as functional fibre sources, further accelerating adoption. As sustainability and health concerns converge, plant derivatives are gaining strategic importance beyond filler roles. Plant derivatives are no longer limited to carbohydrates but include high-value functional ingredients that support digestion, immunity and coat health. Ingredients like chicory root, inulin p, pumpkin flaxseed and blueberry extract are now standard in premium formulations. The European Food Safety Authority has approved health claims for certain plant extracts, such as cranberry for urinary health and turmeric for joint support. Besides, EU organic regulations permit specific plant-based additives in certified organic pet foods c,, creating a premium niche. Brands highlight regional European botanicals such as elderberry and sea buckthorn, appealing to eco-conscious consumers. This functional evolution transforms plant derivatives from cost-saving ingredients into innovation drivers aligned with Europe’s clean label and wellness trends.

REGIONAL ANALYSIS

Germany Market Analysis

Germany dominated the European pet food ingredient market and occupied a 22.7% share in 2024. The leading position of the German market is driven by its large pet population, stringent feed regulations, and strong premium pet food manufacturing base. Germany enforces some of the EU’s strictest ingredient traceability rules under the Feed Hygiene Ordinance, requiring full documentation from farm to factory. The Federal Institute for Risk Assessment conducts regular audits of pet food additives ,, ensuring compliance with EFSA standards. Major manufacturers invest heavily in R&D for functional and hypoallergenic formulas using EU-sourced poultry and plant proteins. Additionally, Germany’s strong organic movement drives demand for certified organic pet foods, which has grown. Germany leads Europe in ingredient quality and innovation, driven by its affluent populace, strict regulations, and discerning consumers.

United Kingdom Market Analysis

The United Kingdom was the next prominent player in the European pet food ingredient market by capturing a 17.8% share in 2024. The growth of the UK market was driven by high pet ownership rates and a mature premium pet care culture. According to sources, a notable share of UK households owned a pet in 2023, with millions of dogs and cats. British consumers are among Europe’s most willing to pay for premium nutrition. Brands emphasise human-grade eats and locally sourced vegetable,, appealing to clean label demand. Additionally, the UK’s strong veterinary sector promotes therapeutic diets with specialised ingredients for kidney and joint health. Despite Brexit, the UK remains deeply integrated into European supply chains and regulatory frameworks, sustaining its influence as a high-value market.

France Market Analysis

France is growing steadily in the European pet food ingredient market due to its large rural pet population, strong agricultural sector, and growing urban cat ownership. According to research, millions of pets were owned in 2023, with cats surpassing dogs in urban centres like Paris and Lyon. France is Europe’s largest poultry producer,, supplying high-quality chicken and duck proteins to domestic and EU pet food makers. The French Ministry of Agriculture enforces strict controls on animal by-product use in feed under the Rural Code a,, aligning with EU standards. Premium brands like Croq’ la Vie and Ultra Premium Direct highlight traceable French meats and regional botanicals such as lavender and rosemary. Additionally, France’s strong organic sector, with annual growth in organic pet food, supports demand for certified plant-based and additive-free formulations. This blend of agricultural abundance and consumer patriotism sustains France’s robust ingredient market.

Italy Market Analysis

Italy experienced gradual growth in the European pet food ingredient market owing to its cultural affinity for pets, high meat consumption, and rising demand for natural diets. It is a major producer of beef, lamb, and fish—key protein sources for premium pet foods. The Italian Ministry of Health mandates that all pet food ingredients comply with EU Regulation 767/20,09, with additional national controls on imported proteins. Brands emphasise Mediterranean ingredients such as olive oils, arugula and artichokes, aligning with regional identity and health trends. Additionally, Italy’s strong small and medium enterprise sector supports artisanal pet food producers who source directly from local farms, enhancing traceability. Italy’s love for food and pets fosters an ingredient market prioritising authentic flavflavour and sensoryeal.

Spain Market Analysis

Spain is predicted to expand in the European food ingredient market from 2025 to 2033 due to rising pet ownership, sun-driven demand for antioxidant-rich diets, and robust agricultural output. It is Europe’s largest producer of olive oil and a major source of poultry and rabbit meat—ingredients increasingly used in premium pet foods for their digestibility and omega-9 content. The Spanish Agency for Food Safety enforces EU feed regulations with additional emphasis on mycotoxin testing due to Mediterranean climate risks. Brands highlight Iberian pork and olive polyphenols as functional ingredients supported by local research from the University of Barcelona. Additionally, Spain’s warm climate drives demand for hydrating wet foods and antioxidant-rich formulas to combat oxidative stress. This synergy of climate agriculture and consumer trends positions Spain as a dynamic and growing ingredient market in Southern Europe.

COMPETITIVE LANDSCAPE

The European pet food ingredient market features intense competition among global nutrition leaders, European agri processors, and specialised functional ingredient innovators. The landscape is shaped by stringent regulatory oversight, consumer demand for clean label transparency, and the rising importance of sustainability credentials. Competition centres not on price but on scientific validation,raceability and alignment with premium pet food trends such as grgrain-freeovel protein and therapeutic nutrition. Large players leverage scale and regulatory expertise to dominate animal protein and vitamin segments, while smaller firms differentiate through niche botanicals, probiotics, or upcycled ingredients. The market remains highly fragmented with no single supplier controlling all categories, yet trust, scientific backing and compliance capability are critical success factors. As pet humanisation accelerates and the EU tightens rules on deforestation and novel ingredient suppliers must balance innovation with rigorous safety and sustainability documentation. This environment favours well-capitalised companies that can navigate regulatory complexity while delivering measurable health and environmental benefits.

KEY MARKET PLAYERS

A few of the market players in the European pet food ingredient market include

- Nestle Purina PetCare (US)

- Mars Petcare (US)

- Hill’s Pet Nutrition (US)

- Diamond Pet Foods (US)

- Blue Buffalo (US)

- Spectrum Brands (US)

- WellPet (US)

- Merrick Pet Care (US)

- Royal Canin (FR)

Top Players in the Market

- Ingredion Incorporated is a global ingredient solutions provider with a significant footprint in the European food ingredient market through its plant-based proteins, starches fibre systems. The company leverages its expertise in grain and pulse processing to deliver clean-label carbohydrate and protein alternatives that align with European clean-label and sustainability trends. Globally, Ingredion contributes to pet nutrition innovation by developing digestibility-enhanced pea and chickpea proteins tailored for canine and feline formulations. In Europe, the company has strengthened its position by achieving EU Novel Food and feed compliance for its pulse proteins and expanding its functional fibre portfolio derived from upcycled fruit and vegetable streams.

- Darling Ingredients Inc. is a leading global supplier of sustainable animal-based ingredients, including rendered proteins, fats and collagen peptides used extensively in European pet food production. The company operates multiple EUEU-based facilities that process food surplus and by-products from the human food chain into high-quality food ingredients under strict EU feed hygiene regulations. Darling contributes to the global market by advancing circular economy practices c,, converting unavoidable food waste into nutritious pet food components. In Europe t,, he company has reinforced its market presence by achieving full compliance with the EU Deforestation Regulation and obtaining certification under the European Pet Food Industry Federation’s sustainability standards.

- BASF SE is a major European chemical and ingredients company that supplies high-purity vitamins C,arotenoi, ds and functional feed additives to the pet food industry across the continent. The company’s portfolio includes essential micronutrients like vitamin E b, beta carotene and omega-3 concentrates derived from sustainable sources that support immune function, skin health and cognitive development in pets. Globally, BASF drives innovation in pet nutrition through its human-grade vitamin production and stability technologies that ensure nutrient retention during extrusion and storage. In Europe, he company has deepened its engagement by aligning its additive portfolio with the European Pet Nutrition Council’s therapeutic guidelines and supporting clinical studies on joint and urinary health.

Top Strategies used by the Key Market Players

Key players in the European pet food ingredient market prioritise regulatory compliance by aligning products with EUthe Feed Hygiene Regulation, EFSA safety dossier,,s and the Farm to Fork Strategy’s sustainability criteria. They invest in traceability systems, including blockchain and QR labels, aiming to meet consumer demand for ingredient transparency. Companies develop functional and therapeutic ingredients that address specific pet health,,th needs such as joint mobility, digestive wellness and urinary health. Strategic partnerships with pet food manufacturers, veterinarians and research institutions enhance scientific credibility and accelerate product validation. Vendors also emphasise circular economy principles by utilising cycled food streams and insect or algae-based proteins to reduce environmental impact. These strategies collectively respond to Europe’s unique convergence of rigorous regulation, health consciousness and sustainability expectations in pet nutrition.

MARKET SEGMENTATION

This research report on the European pet food ingredient market is segmented and sub-segmented into the following categories.

Ingredient Type

- Meat and Meat Products

- Deboned Meat

- Meat Meal

- By-Product Meal

- Animal Digest

- Cereals

- Corn and Corn Meal

- Wheat and Wheat Meal

- Barley

- Rice

- Vegetables and Fruits

- Fruits

- Potato

- Carrots

- Soy and Soymeal

- Pea

- Fats

- Fish Oil

- Lard

- Tallow

- Vegetable Oil

- Poultry Fat

- Additives

- Vitamins and Minerals

- Enzymes

- Other Additives

Form

Product Type

Animal

- Dog

- Cat

- Fish

- Bird

- Rabbit

- Others

Source

- Animal Based

- Plant-Derivatives

- Synthetic

Nature

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link