Europe Organic and Natural Pet Food Market Size

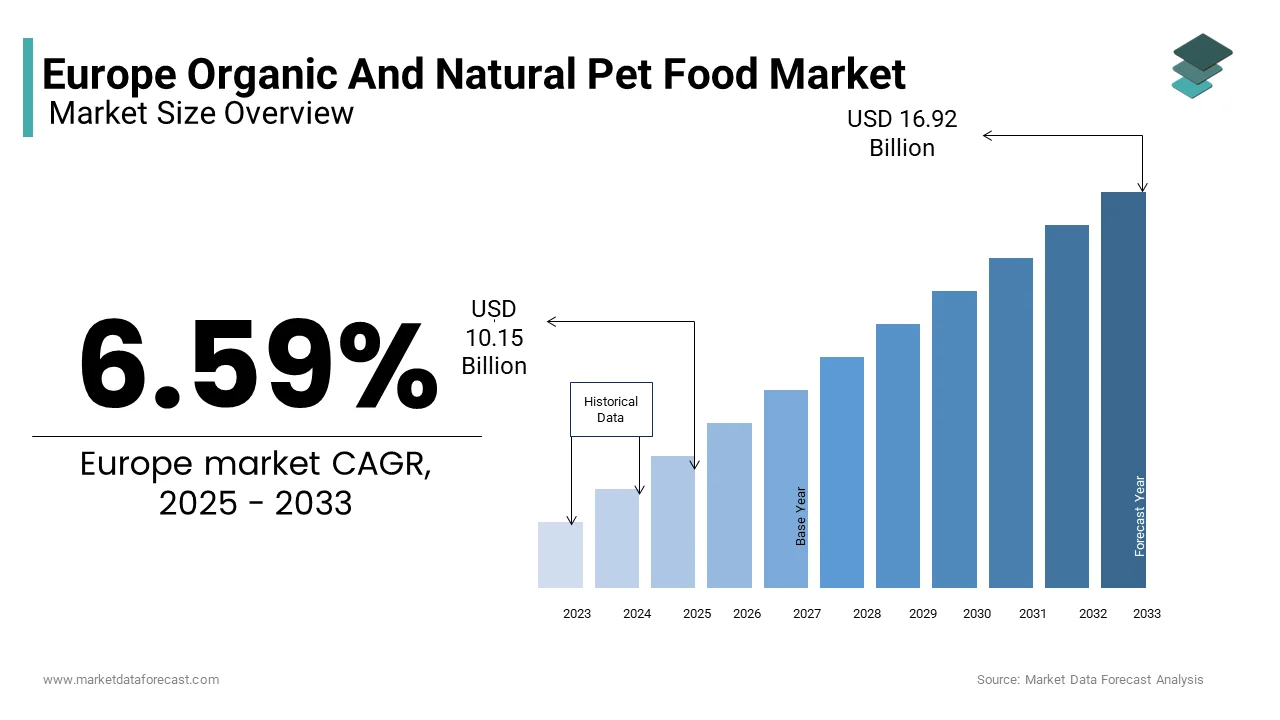

The Europe organic and natural pet food market was valued at USD 9.52 billion in 2024 and is anticipated to reach USD 10.15 billion in 2025 from USD 16.92 billion by 2033, growing at a CAGR of 6.59% during the forecast period from 2025 to 2033.

The Europe organic and natural pet food market focuses on products made from ingredients free from synthetic additives, artificial preservatives, genetically modified organisms (GMOs), and chemical-based pesticides. These products are typically formulated to align with human-grade food standards and emphasize high-quality protein sources, whole-food ingredients, and sustainable sourcing practices. As consumer awareness around animal health and wellness grows, there has been a parallel shift in demand for cleaner, safer, and more ethically produced pet food options.

Europe has emerged as a key region in this sector, particularly in Western European countries such as Germany, France, and the UK. The European Pet Food Industry Federation (FEDIAF) plays a pivotal role in ensuring quality and nutritional adequacy across pet food categories, further reinforcing consumer confidence.

MARKET DRIVERS

Rising Humanization of Pets

One of the most influential drivers behind the growth of the Europe organic and natural pet food market is the increasing humanization of pets. Pet owners across Europe are increasingly treating their animals as family members, leading them to make purchasing decisions based on personal values and health considerations. This trend is particularly pronounced in urban centers where pet ownership has surged and spending per pet has increased accordingly. According to a report by the European Pet Food Industry Federation (FEDIAF), over 80 million households in Europe own at least one pet, and a significant portion of these owners consider their pets as integral members of the family. This mindset directly influences the type of food they choose, favoring organic and natural alternatives that mirror their dietary preferences. Moreover, younger generations—especially millennials—are willing to pay a premium for high-quality pet food products that ensure longevity and better health outcomes for their pets. This behavior is reinforced by the availability of detailed product information online, which allows consumers to compare ingredient transparency and ethical sourcing practices. As a result, brands that align with clean-label trends and offer traceable supply chains are gaining traction.

Increasing Awareness About the Health Benefits of Organic Ingredients

Another major driver fueling the Europe organic and natural pet food market is the growing awareness among pet owners regarding the health benefits associated with organic and natural ingredients. Consumers are becoming more informed about how specific nutrients affect their pets’ immune systems, digestion, skin health, and overall vitality. Scientific studies and veterinary recommendations have highlighted the advantages of organic meat, non-GMO vegetables, and grain-free formulas in reducing allergies and improving energy levels in pets. As a result, many pet owners are shifting away from conventional pet food products laden with artificial additives and fillers. This heightened awareness is being supported by extensive digital campaigns and educational content disseminated through social media platforms, pet forums, and veterinary websites. According to the Pet Food Manufacturers’ Association (PFMA), over 70% of British pet owners consult online resources before making a purchase decision related to pet food. Furthermore, the rise in pet insurance adoption across Europe, particularly in Germany and Sweden, has encouraged pet owners to invest in premium nutrition as part of preventive healthcare strategies.

MARKET RESTRAINTS

High Cost of Organic and Natural Pet Food Products

A major restraint impeding the widespread adoption of organic and natural pet food in Europe is the relatively high cost associated with these products compared to conventional pet food options. Organic certification processes, sustainable sourcing, and limited economies of scale contribute to elevated production expenses, which are ultimately passed on to consumers. This price differential limits accessibility, especially for budget-conscious consumers in Eastern and Southern Europe, where household income levels are comparatively lower. Furthermore, despite the growing awareness of health benefits, affordability remains a critical factor influencing purchasing decisions. While premium brands continue to target affluent segments, mass-market penetration remains challenging without significant reductions in production costs or government-backed subsidies similar to those seen in the human organic food sector. Also, fluctuating raw material prices, particularly for organic meat and plant-based proteins, add another layer of financial uncertainty for manufacturers. As a consequence, many smaller players struggle to compete with established brands, limiting market diversity and innovation potential.

Limited Availability and Distribution Channels

Another significant challenge facing the Europe organic and natural pet food market is the limited availability and fragmented distribution network, especially in rural and less developed regions. Unlike traditional pet food products that benefit from well-established retail channels, organic and natural variants often rely on niche specialty stores, online retailers, and direct-to-consumer models, which restrict their reach. This disparity is partly due to logistical complexities and higher inventory costs associated with maintaining fresh, perishable, or minimally processed ingredients. Moreover, small and mid-sized organic pet food manufacturers face difficulties in securing shelf space in supermarket chains, which tend to prioritize established brands with broader distribution capabilities. Besides, cross-border distribution within the EU faces regulatory variations and labeling requirements that complicate expansion efforts for local producers. These constraints hinder market penetration and limit consumer exposure, especially in regions where awareness and education about organic pet nutrition remain low.

MARKET OPPORTUNITY

Expansion of E-Commerce Platforms Specializing in Premium Pet Products

One of the most promising opportunities for the Europe organic and natural pet food market lies in the rapid expansion of e-commerce platforms specializing in premium pet products. The digital transformation of retail has enabled niche brands to bypass traditional distribution barriers and connect directly with health-conscious pet owners. Online marketplaces dedicated to pet care, such as Zooplus AG in Germany and Yora in the UK, have reported substantial growth in recent years, offering curated selections of organic and natural pet foods that cater to evolving consumer preferences. E-commerce provides several advantages, including personalized shopping experiences, detailed product descriptions, and customer reviews that help build trust and brand loyalty. This is particularly beneficial for organic and natural pet food brands that rely on transparency and ingredient traceability to attract discerning buyers. Also, subscription-based models offered by online retailers ensure regular replenishment, enhancing customer retention and repeat purchases. As internet penetration increases and digital payment systems become more secure across Europe, especially in emerging markets like Poland and Romania, the e-commerce channel presents a scalable avenue for organic pet food brands to expand their footprint.

Innovation in Sustainable Packaging and Eco-Friendly Formulations

Another significant opportunity driving the Europe organic and natural pet food market is the increasing focus on sustainability through innovative packaging solutions and eco-friendly product formulations. With environmental concerns gaining prominence across the continent, pet food manufacturers are under pressure to reduce their carbon footprint and align with circular economy principles. According to a report by the European Environment Agency, over 65% of consumers in Scandinavia and Benelux prioritize sustainability when purchasing pet-related products, signaling a strong market pull for greener alternatives. Leading companies are responding by introducing biodegradable bags, recyclable containers, and compostable pouches to package their organic pet food lines. Such initiatives not only appeal to environmentally conscious consumers but also enhance brand reputation and compliance with upcoming EU regulations on plastic waste reduction. Apart from these, some manufacturers are experimenting with insect-based protein and algae-derived ingredients to create nutrient-rich, low-impact pet food formulas. Research from Wageningen University indicates that insect protein requires less land and emits fewer greenhouse gases compared to traditional livestock farming. These innovations resonate strongly with younger, urban pet owners who value both pet health and planetary well-being.

MARKET CHALLENGES

Regulatory Complexity and Labeling Standards Across EU Member States

A major challenge confronting the Europe organic and natural pet food market is the regulatory complexity and inconsistent labeling standards across EU member states. Although the European Commission and FEDIAF have established broad guidelines for pet food safety and composition, individual countries maintain varying interpretations and enforcement mechanisms, creating compliance hurdles for manufacturers. These inconsistencies not only delay product launches but also increase operational costs due to the need for customized formulations and packaging for different markets. A study by the European Pet Food Industry Association (EPFIA) found that small and medium-sized enterprises (SMEs) spend more on compliance and certification processes compared to multinational corporations with dedicated legal teams. In addition, unclear or ambiguous labeling requirements often mislead consumers, eroding trust in organic claims. Harmonizing these regulations across the EU would streamline market access and foster greater transparency, but until then, regulatory fragmentation remains a persistent barrier to uniform growth and scalability in the organic and natural pet food sector.

Consumer Misunderstanding and Greenwashing Concerns

Another pressing challenge affecting the Europe organic and natural pet food market is the prevalence of consumer misunderstanding and greenwashing concerns. Despite rising awareness about organic and natural pet food benefits, many consumers still struggle to differentiate between genuine organic certifications and misleading marketing claims. Terms like “natural,” “wholesome,” and “clean” are frequently used without clear regulatory backing, leading to confusion and skepticism among buyers. Greenwashing, where brands exaggerate or falsely claim sustainability credentials, has further complicated the landscape. Several pet food manufacturers have faced scrutiny from watchdog groups and consumer advocacy organizations for using vague terms like “eco-friendly” or “green” without verifiable evidence. In response, the European Parliament proposed stricter advertising regulations in early 2024 aimed at curbing deceptive environmental claims, which could impose additional compliance burdens on pet food marketers. Meanwhile, consumer trust remains fragile; a survey by YouGov found that only 35% of UK pet owners fully trust organic pet food branding, citing concerns about authenticity and price justification. To combat this issue, industry stakeholders are calling for standardized labeling frameworks and third-party verification systems.

REPORT COVERAGE

|

REPORT METRIC |

DETAILS |

|

Market Size Available |

2024 to 2033 |

|

Base Year |

2024 |

|

Forecast Period |

2025 to 2033 |

|

CAGR |

6.59% |

|

Segments Covered |

By Pet Type, Product Type, Packaging Ty,pe And By Country |

|

Various Analyses Covered |

Global, Regional & Country Level Analysis; Segment-Level Analysis, DROC, PESTLE Analysis, Porter’s Five Forces Analysis, Competitive Landscape, Analyst Overview of Investment Opportunities |

|

Regions Covered |

UK, France, Spain, Germany, Italy, Russia, Sweden, Denmark, Switzerland, Netherlands, Turkey, Czech Republic & Rest of Europe |

|

Market Leaders Profiled |

PetGuard Holdings, LLC, Nestlé Purina Pet Care (Nestlé Holdings, Inc.), Newman’s Own, Evanger’s Dog & Cat Food Company, Inc, Lily’s Kitchen (Nestle Purina PetCare), Avian Organics, Castor & Pollux Natural Petworks (Merrick Pet Care, Inc.), Yarrah (AAC Capital). |

SEGMENTAL ANALYSIS

By Pet Type insights

The dog food segment dominated the Europe organic and natural pet food market by accounting for 58.6% of total sales in 2024. This leading position is primarily driven by the high prevalence of dog ownership across the continent and a growing consumer preference for premium nutrition tailored to canine health needs. The emotional attachment between owners and their pets has significantly influenced purchasing behavior, particularly among urban millennials who view dogs as family members. Additionally, increasing awareness about breed-specific dietary requirements and chronic conditions such as allergies and digestive issues has led pet parents to seek out high-quality, organic formulations. Furthermore, industry players have responded to this demand by launching innovative products such as raw-based diets, freeze-dried meals, and ethically sourced meat blends, further boosting market penetration.

On the other hand, the cat food segment is anticipated to register the highest CAGR of 9.6% during the forecast period. This accelerated growth is attributed to rising cat adoption rates and shifting perceptions around feline nutrition. Unlike previous years, where cats were often considered low-maintenance pets, there is now a growing emphasis on specialized dietary care, including hypoallergenic formulas and urinary tract support ingredients. Moreover, the influence of social media and online veterinary resources has empowered cat owners to make informed decisions regarding their pets’ diets. In addition, convenience-driven product formats such as single-serve pouches and functional treats have enhanced appeal among time-constrained consumers. Online retailers like Zooplus AG reported a key increase in organic cat food orders in 2023, reflecting the expanding digital footprint of this segment.

By Product Type Insights

The dry pet food remained the largest segment in the Europe organic and natural pet food market by holding an estimated 52.1% of total volume in 2024. This dominance can be attributed to its long shelf life, cost-effectiveness, and ease of storage, making it a preferred choice for budget-conscious yet quality-oriented pet owners. Moreover, dry food is widely associated with dental benefits, especially in dogs, due to its abrasive texture that helps reduce plaque buildup. In addition, advancements in extrusion technology have enabled manufacturers to produce nutrient-dense organic dry food without compromising on taste or digestibility. Brands such as Anifit and Wolfsblut have introduced organic dry formulations enriched with superfoods like chia seeds, cranberries, and flaxseed, catering to evolving consumer expectations. Furthermore, e-commerce platforms have expanded access to niche dry food brands, allowing smaller players to compete effectively.

Snacks and treats represented the fastest advancing product type within the Europe organic and natural pet food market, projected to rise at a CAGR of 10.4% through 2033. This rapid expansion is fueled by the rising trend of indulgence-based pet feeding, where owners use treats not only for training but also as expressions of affection. Furthermore, functional treats—those infused with joint-supporting glucosamine, calming CBD extracts, or digestion-enhancing probiotics—are becoming mainstream offerings. The Pet Food Manufacturers’ Association (PFMA) reports that functional treats accounted for a significant portion of new organic pet snack launches in the UK. In tandem, the humanization of pets has prompted manufacturers to develop gourmet-style treats made from free-range meats, organic vegetables, and even vegan alternatives. E-commerce has also played a pivotal role in driving this segment’s growth, as online platforms allow for greater product variety and targeted marketing.

By Packaging Type Insights

The bags continued to be the prominent packaging format in the Europe organic and natural pet food market by capturing 48.2% of total sales in 2024. This is due to the practical advantages offered by bag packaging, including resealability, lightweight design, and efficient storage, particularly for dry food products. Also, major retail chains across Germany, France, and the Netherlands favor bagged pet food for their logistics-friendly bulk handling and stacking capabilities. Furthermore, direct-to-consumer brands leverage flexible packaging to offer subscription-based models that enhance customer retention and convenience. Consumer preference for portion-controlled and easy-to-pour packaging also contributes to the segment’s strength. As sustainability concerns mount, several companies, including UK-based OmNom and Swiss firm NutriNord, have introduced recyclable and biodegradable bag options, aligning with regulatory shifts and consumer values.

The pouches are emerging as the quickest rising packaging type in the Europe organic and natural pet food market, predicted to expand at a CAGR of 11.2% over the years. This is primarily driven by their suitability for wet and semi-moist formulations, which are gaining traction due to their palatability and hydration benefits. The convenience factor is a key driver behind the pouch format’s popularity. Pet parents appreciate the portability, mess-free dispensing, and portion control features of pouches, especially when traveling or feeding small or senior animals. Moreover, brands are leveraging stand-up pouches with tear-notches and resealable zippers to improve user experience and shelf appeal. Sustainability initiatives are also influencing this shift. Several pouch manufacturers are adopting mono-material structures that facilitate recycling, addressing environmental concerns linked to multi-layered plastics.

COUNTRY ANALYSIS

Germany held the top position in the Europe organic and natural pet food market by commanding an 18.5% share in 2024. This is underpinned by a robust pet ownership culture, high disposable incomes, and stringent regulatory standards enforced by the Federal Ministry of Food and Agriculture (BMEL). According to FEDIAF, Germany is home to approximately 10.6 million dogs and over 14 million cats, making it one of the largest pet-owning nations in Europe. German consumers exhibit a strong preference for premium, transparently labeled pet food products, with a key portion of pet owners considering ingredient quality before making a purchase decision. Additionally, the country’s advanced retail infrastructure and well-established e-commerce ecosystem support widespread availability of organic pet food. Platforms like zooplus.de and Amazon Pet Supplies have played a crucial role in expanding access to niche brands. Moreover, Germany’s commitment to animal welfare and environmental sustainability has spurred demand for certified organic and cruelty-free pet food. The government-backed “Bio” certification system ensures strict compliance with organic farming standards, reinforcing consumer trust.

The French market benefits from a growing pet population, increasing urbanization, and a cultural inclination toward health-conscious consumption. Also, pet ownership in France exceeds 28 million domestic animals, with dogs and cats being the most common companions. A key driver of growth is the rising influence of millennial pet owners who prioritize ethical sourcing and nutritional transparency. This trend is further reinforced by government policies promoting sustainable agriculture and organic livestock production, which indirectly support the availability of high-quality pet food ingredients. French consumers also show a strong affinity for premium and locally produced pet food brands. Companies like Virbac and Almo Nature have capitalized on this sentiment by offering regionally sourced, organic pet food lines. Meanwhile, e-commerce growth, particularly through platforms like Zooplus.fr and Amazon France, has broadened access to specialty products.

The United Kingdom holds a prominent position in the Europe organic and natural pet food market. Despite economic headwinds following Brexit and inflationary pressures, the UK maintains a resilient market driven by deep-rooted pet ownership traditions and high consumer awareness around pet wellness. British consumers are particularly discerning when it comes to pet food quality, often scrutinizing ingredient lists and ethical sourcing claims. This mindset has encouraged domestic brands like Yora and Lily’s Kitchen to focus on clean-label formulations and sustainable supply chains. Besides, the UK’s progressive stance on alternative proteins has fostered innovation in insect-based and plant-powered pet food solutions. Regulatory clarity from the Department for Environment, Food & Rural Affairs (DEFRA) has further facilitated the introduction of novel ingredients into the market. Coupled with a well-developed online retail network, the UK remains a key growth engine for organic and natural pet food brands across Europe.

Italy occupies a major share of the market. The market is characterized by a deeply ingrained pet culture, where pets are often considered integral family members, especially among urban households. One of the primary drivers of growth is the increasing alignment between human and pet food trends. Italian consumers place a high value on food quality, authenticity, and regional sourcing, which translates into strong demand for organic pet food products with recognizable ingredients. A 2023 survey by Nomisma reveals that 47% of Italian pet owners associate organic pet food with superior digestibility and skin health, prompting them to switch from conventional brands. Moreover, the presence of influential domestic players such as Farmina Pet Foods and Almo Nature has bolstered market confidence by offering premium, grain-free, and certified organic formulations. These brands emphasize Mediterranean-inspired diets rich in fish, legumes, and olive oil derivatives, resonating well with local tastes. Additionally, Italy’s active participation in EU-wide sustainability initiatives has strengthened the case for eco-friendly packaging and responsible sourcing practices, further enhancing the appeal of organic pet food offerings.

Spain has emerged as a rapidly growing market due to increasing pet adoption rates, especially in urban centers like Madrid and Barcelona. A key growth catalyst is the rise in dual-income households and single-person dwellings, where pets serve as emotional companions. This shift is being supported by aggressive digital marketing campaigns and influencer endorsements that highlight the health benefits of organic ingredients. Moreover, Spain’s agricultural sector provides a reliable source of organic raw materials, facilitating the development of domestically produced pet food brands. Companies like Sí! Pure Petfood has leveraged this advantage to launch organic, refrigerated pet meals that cater to health-conscious buyers. As e-commerce expands and pet insurance gains traction, Spain is poised to become a more influential player in the European organic and natural pet food market in the coming years.

KEY MARKET PLAYERS

PetGuard Holdings, LLC, Nestlé Purina Pet Care (Nestlé Holdings, Inc.), Newman’s Own, Evanger’s Dog & Cat Food Company, Inc, Lily’s Kitchen (Nestle Purina PetCare), Avian Organics, Castor & Pollux Natural Petworks (Merrick Pet Care, Inc.), Yarrah (AAC Capital). are the market players that are dominating the Europe organic and natural pet food market.

Top Players In The Market

One of the leading players in the Europe organic and natural pet food market is Nestlé Purina PetCare. The company has consistently demonstrated a strong commitment to offering premium, health-focused pet nutrition solutions. With a wide range of certified organic and natural pet food products, Nestlé Purina has built a reputation for quality and innovation. Its emphasis on research-backed formulations and sustainable sourcing has enabled it to maintain consumer trust across key European markets. By leveraging its global distribution network and deep understanding of pet owner behavior, the company plays a pivotal role in shaping industry standards and influencing product development trends.

Another major player is Hill’s Pet Nutrition, known for its science-driven approach to pet wellness. Hill’s has successfully integrated organic and natural ingredients into many of its premium product lines, catering to the growing demand for clean-label pet food. The brand’s association with veterinary professionals enhances its credibility among pet owners seeking expert-recommended diets. In Europe, Hill’s has focused on expanding its presence through strategic retail partnerships and digital engagement strategies that emphasize ingredient transparency and nutritional benefits. This approach has allowed the company to solidify its position as a trusted name in the organic and natural pet food segment.

Smalls Pet Food, though relatively new compared to industry giants, has quickly gained traction in the European market by focusing exclusively on high-quality, human-grade organic pet food. The company operates on a direct-to-consumer model, allowing for greater control over product freshness and customer experience. Smalls emphasizes minimal processing, ethically sourced meats, and transparent supply chains, which resonate strongly with modern pet owners. Its subscription-based service ensures consistent availability and personalized feeding plans, contributing to customer loyalty and brand differentiation. As awareness around holistic pet care continues to rise, Smalls is emerging as a formidable contender in the European organic and natural pet food landscape.

Top Strategies Used By Key Market Participants

A primary strategy employed by key players in the Europe organic and natural pet food market is product innovation and diversification. Companies are continuously launching new formulations that align with evolving consumer preferences, including grain-free, insect-based, and plant-powered options. These innovations not only cater to specific dietary needs but also differentiate brands in a highly competitive environment. By investing in research and development, manufacturers ensure their offerings remain relevant and appealing to health-conscious pet owners.

Another critical strategy is expanding digital presence and e-commerce capabilities. As online shopping becomes the preferred purchasing channel for many consumers, companies are strengthening their digital infrastructure. This includes optimizing websites, enhancing mobile apps, and partnering with online pet retailers to improve accessibility and convenience. Direct-to-consumer models have gained popularity, enabling brands to build stronger relationships with pet parents while collecting valuable insights for future product development.

Lastly, strategic collaborations and acquisitions play a significant role in market expansion. Established players often acquire niche or regional brands to enhance their product portfolios and geographic reach. Additionally, partnerships with veterinarians, influencers, and pet wellness platforms help reinforce brand credibility and drive consumer trust. These moves enable companies to strengthen their foothold and respond effectively to shifting market dynamics.

COMPETITION OVERVIEW

The competition in the Europe organic and natural pet food market is characterized by a dynamic blend of established multinational corporations and emerging niche players, all vying for a share of a rapidly expanding sector. As consumer expectations evolve toward cleaner, more sustainable, and ethically sourced ingredients, brands are under increasing pressure to innovate and differentiate themselves. While large-scale manufacturers benefit from extensive distribution networks and strong brand recognition, smaller, specialized firms are gaining traction by offering unique formulations and emphasizing transparency in sourcing and production practices. The market is witnessing a surge in private label entries from major supermarket chains, further intensifying the battle for shelf space and consumer loyalty. Digital marketing, especially through social media and influencer partnerships, has become a crucial battleground for brand visibility and customer engagement. Moreover, sustainability initiatives such as eco-friendly packaging and carbon-neutral operations are increasingly influencing purchasing decisions. This heightened level of competition is driving continuous improvements in product quality, formulation transparency, and overall consumer experience, making the European market one of the most progressive and competitive in the global pet food industry.

RECENT HAPPENINGS IN THE MARKET

- In February 2024, Nestlé Purina PetCare launched a new line of organic cat food made with free-range poultry and sustainably sourced fish, targeting environmentally conscious pet owners across Western Europe.

- In June 2024, Hill’s Pet Nutrition introduced a digital platform that provides pet owners with personalized feeding recommendations based on breed, age, and health conditions, enhancing engagement and reinforcing brand trust.

- In September 2024, Smalls Pet Food expanded its direct-to-consumer delivery service to Germany and France, aiming to capitalize on the rising demand for fresh, human-grade organic pet meals in these markets.

- In November 2024, a strategic partnership was formed between Lily’s Kitchen and a UK-based animal wellness startup to develop functional treats infused with adaptogens and probiotics, supporting digestive and emotional health in pets.

- In March 2025, Yora, a UK-based organic pet food brand, introduced a fully recyclable insect-protein-based dog food pouch, reinforcing its commitment to sustainability and addressing environmental concerns within the pet food industry.

MARKET SEGMENTATION

This research report on the Europe organic and natural pet food market is segmented and sub-segmented into the following categories.

By Pet Type

By Product Type

- Dry Pet Food

- Wet and Canned Pet Food

- Snacks and Treats

By Packaging Type

- Bags

- Cans

- Pouches

- Boxes

- Others

By Country

- UK

- France

- Spain

- Germany

- Italy

- Russia

- Sweden

- Denmark

- Switzerland

- Netherlands

- Turkey

- Czech Republic

- Rest of Europe

link